Understanding tokenization and real world assets

The DeFi <> TradFi convergence thats bringing trillions in assets onchain.

There's used to be narrative in crypto that was about tokenizing everything, putting it onchain, and watching the old financial system crumble. At the early stages of DeFi it was certainly a rallying cry, today its also completely wrong.

What's actually happening is messier, more interesting, and frankly more bullish than the "tokenize the world" meme suggests.

In the most simple terms, tokenization is forcing a convergence between two financial architectures. Let's talk about what that convergence actually looks like, where the friction points are, and why this matters more than almost anything else happening in crypto right now.

How the tokenization landscape has changed

In 2017 there were several RWA experiments, many of which were before their time. Why? these projects failed to execute or have clarity on the elements that really matter.

- Immature infrastructure

- No institutional custod

- No regulatory clarity

- No real settlement layer.

Fast forward to 2026 and the landscape with respect to these elements is almost unrecognizable.

Stablecoins have become legitimate settlement assets processing hundreds of billions in volume. Onchain market microstructure has matured to the point where it can handle real capital. Institutional custody solutions exist from players like Anchorage and Fireblocks. And maybe most importantly, regulators, are actively opening doors through legislation like the GENIUS Act and the CLARITY Act.

When BlackRock's Larry Fink writes about tokenization as the future of financial markets, and SEC Chairman Paul Atkins predicts U.S. financial markets could move onchain "within two years," “tokenizing the world” has gone from a meme to a very probable future in less than 10 years, albeit probably not how crypto OGs first imagined.

Not all RWAs are created equal

For better or worse, the industry, at this point, has coalesced on the term “RWA”. Regardless of the terminology, the industry treats RWAs as a monolithic category, and that is simply not reality.

"Tokenized real-world assets" gets thrown around as if putting a Treasury bill onchain is the same technical and regulatory challenge as putting a private credit facility onchain.

- Rights defines what you actually own when you hold the token. Is it synthetic exposure (you're basically betting on a price, like a perpetual future)? A contractual claim on something held offchain (a receipt token)? Or direct digital ownership of the asset itself?

- Settlement defines where the transaction actually finalizes. Does it settle through traditional finance rails while using the blockchain as a fancy spreadsheet? Or does it settle entirely onchain through smart contracts?

These two axes create four distinct models, and each one has radically different implications for composability, regulation, and who captures the value.

The four models of onchain RWAs

Model 1: Synthetic derivatives

Protocols like Hyperliquid, Ostium, and Lighter create perpetual futures or prediction markets that track real-world asset prices through oracles. In this model, you as a token holder down “own” anything with respect to the underlying, you own price exposure.

For many, this is the fastest path to marke - no custody, no regulatory wrapper around actual securities. You get 24/7 trading, instant settlement, and global access. The tradeoff is that you have zero ownership rights and you're dependent on oracle infrastructure. Prediction market and RWA perpetual volumes have grown substantially, proving there's real demand for this model.

Model 2: Wrapped assets

A regulated entity holds the actual asset offchain and issues a receipt token onchain. To date, this is where the big institutional money is playing. Ondo's OUSG (tokenized short-term Treasuries), Franklin Templeton's BENJI fund, or Dinari's tokenized stocks are all great examples.

This model dominates treasuries and money markets for good reason the Federal Reserve's book-entry system is deeply entrenched, and no one is going to bypass it anytime soon. But wrapped assets unlock something powerful: DeFi composability. Once a Treasury position is a token, it can be used as collateral, traded in AMMs, and integrated into yield strategies. That's genuinely new.

https://app.rwa.xyz/treasuries

Model 3: Collateralized borrowing

In this model RWAs serve as collateral for onchain stablecoin debt. MakerDAO (now Sky) has been doing it with RWA vaults, Figure Markets is tokenizing HELOCs.

This model is elegant because it doesn't require the asset itself to move onchain - just the collateral relationship. It bridges the two worlds without requiring either to fundamentally change - providing benefits like scalability and reliable yield for onchain native users.

Model 4: Primary onchain issuance

Securities created directly on blockchain as native tokens, with the chain as the official record. This is the endgame for programmable compliance, real-time settlement and instant clearing. It's also the model with the most regulatory friction.

For private credit, this is where things get interesting. As lending infrastructure matures, there's a clear path for loans to originate directly onchain, with programmable terms, automated payments, and transparent risk assessment.

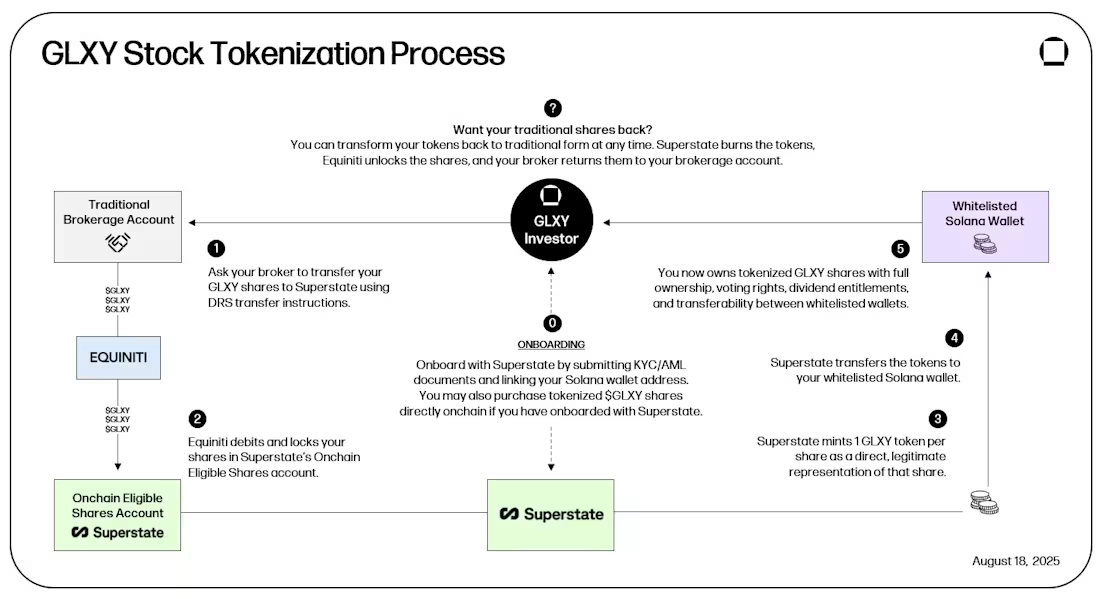

https://www.galaxy.com/insights/research/tokenized-glxy

Frictions that RWA and tokenization still face

Even though RWAs have made great progress, there are still very real friction points that will stall adoption and growth:

- Regulatory arbitrage vs. regulatory clarity: DeFi's permissionless nature is its superpower and its biggest obstacle. The GENIUS Act and CLARITY Act signal regulatory willingness to engage, but the details matter enormously.

- 24/7 vs. business hours: Although RWAs may “trade” 24/7, redemptions can be significantly dependand on offchain liquidity. With some RWAs still facing a 30-60-or even 90 day redemption period. When BlackRock's tokenized fund needs to settle against an AMM pool, whose clock wins?

- Custody assumptions: DeFi assumes self-custody as the default, while tradFi requires institutional custody as the requirement. Bridging this gap without compromising the benefits of either system is an unsolved problem for most asset classes.

- Oracle dependency: Every RWA model except primary onchain issuance depends on oracles to connect the onchain representation to the offchain reality. This is a single point of failure that the industry hasn't fully addressed. Accessing RWA markets onchain is no more streamlined that investing in an offchain product. There are still 3-6 week KYC/KYB onboarding processes, and strict controls over what you can do with those assets once purchased.

Points of promise

Despite the friction, certain convergence points are accelerating faster than anyone expected:

- Stablecoins as the settlement layer: This is the most underappreciated development. Stablecoins aren't just a crypto thing anymore, they're becoming the neutral settlement infrastructure that both systems can agree on. When a tokenized Treasury settles in USDC, both DeFi and TradFi can process it.

- Private credit going onchain: This is the second-fastest growing RWA category, and it makes sense, private credit is already opaque, illiquid, and manually processed. Moving it onchain actually solves real problems around transparency, tranching efficiency, and secondary market liquidity.

- Institutional infrastructure: The build-out of institutional-grade custody, compliance, and market-making infrastructure means that the "but institutions can't use this" objection is rapidly disappearing.

Whats next for RWAs and tokenization

We're not heading toward a world where traditional finance is replaced by DeFi, we're heading toward a world where there is a clear convergence that is mutually beneficial.

The assets are real and of substance, the rails are programmable, the settlement is onchain, everything is compliant and the custody is institutional. None of these things contradict each other, they're just components of a new financial system that doesn't fit neatly into either the "DeFi" or "TradFi" box.

The projects and protocols that understand this:

- Superstate building tokenization infrastructure

- Ondo bridging institutional money markets into DeFi composability

- Centrifuge channeling real credit into onchain structures

All of these players are not doing "crypto stuff" or "TradFi stuff." They're doing finance, simply. using the best technology available for each layer of the stack. It just so happens that blockchains are a fundamental piece of that.

For yield seekers onchain, this convergence is enormously consequential. Every tokenized Treasury, every onchain credit facility, every synthetic RWA market creates new yield opportunities that didn't exist before and more importantly, they create yield that's backed by real economic activity, not just recursive DeFi token emissions.

Where Summer.fi Institutional fits in

Summer.fi is launching a permissioned RWA Vault built for institutions, hedge funds, and custodians ready to put idle treasury capital to work.

Actively managed by digital hedge fund M1 Capital, the vault dynamically rebalances across the highest-quality tokenized assets and private credit markets, aggregating deep-liquidity yield sources into a single, contagion-free strategy.

Every dollar is ring-fenced. strictly isolated smart contracts ensure zero commingling of funds, while integration with trusted custody partners Utila and Balance keeps the compliance and operational overhead low.